Missed Filing Form 5472? The Complete 2026 Catch-Up Guide

Missed Form 5472 for your foreign-owned US LLC? Avoid the $25,000 IRS penalty. Learn how to use the DIIRSP process and write a winning reasonable cause statement.

Finvio Editorial Team

Foreign-Owned LLC Compliance Research

•13 min read •Includes reasonable cause statement template

Quick Answer

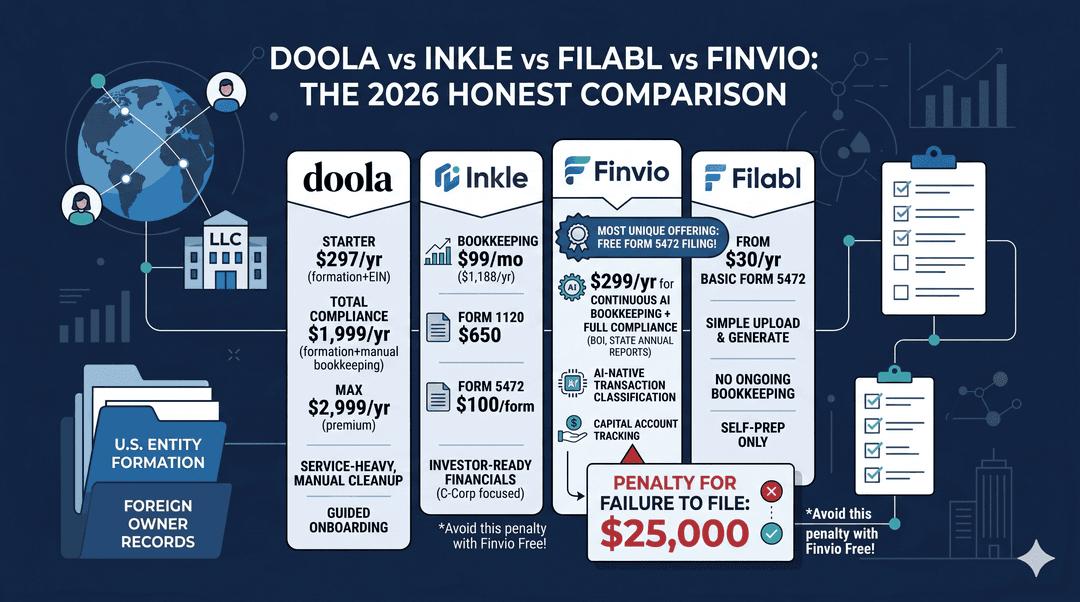

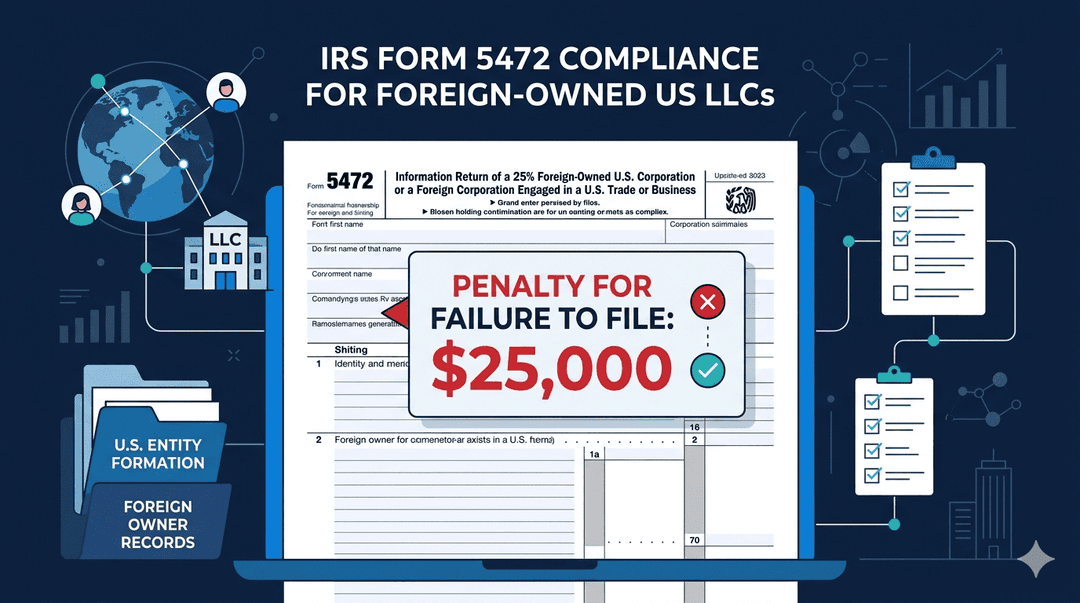

If you missed filing Form 5472 for your foreign-owned US LLC, you may qualify for $0 in penalties under the IRS Delinquent International Information Return Submission Procedure (DIIRSP), but only if you file before the IRS contacts you. The standard penalty is $25,000 per missed form, per year, with additional $25,000 stacking every 30 days after a 90-day IRS notice period. However, the IRS routinely accepts reasonable cause statements that establish you exercised ordinary business care and prudence and your failure was due to circumstances beyond your control. The earlier you file, the higher your chance of penalty relief.

⚠ Critical timing rule: Once the IRS sends an inquiry letter about a missed filing, your relief options drop dramatically. Filing proactively — before any IRS contact — is the single most important factor in avoiding penalties.

The fear is real, but the situation is fixable

If you've just realized you owe Form 5472 for prior years, you're not alone. Thousands of foreign founders discover this obligation 1-7 years after forming their US LLC, usually when:

- A Reddit comment mentions the $25,000 penalty

- A new CPA reviews their books

- A friend tells them about the rule

- They Google "do I need to file taxes for my US LLC" for the first time

The fear is rational. The IRS treats Form 5472 penalties seriously, and the dollar amounts are catastrophic.

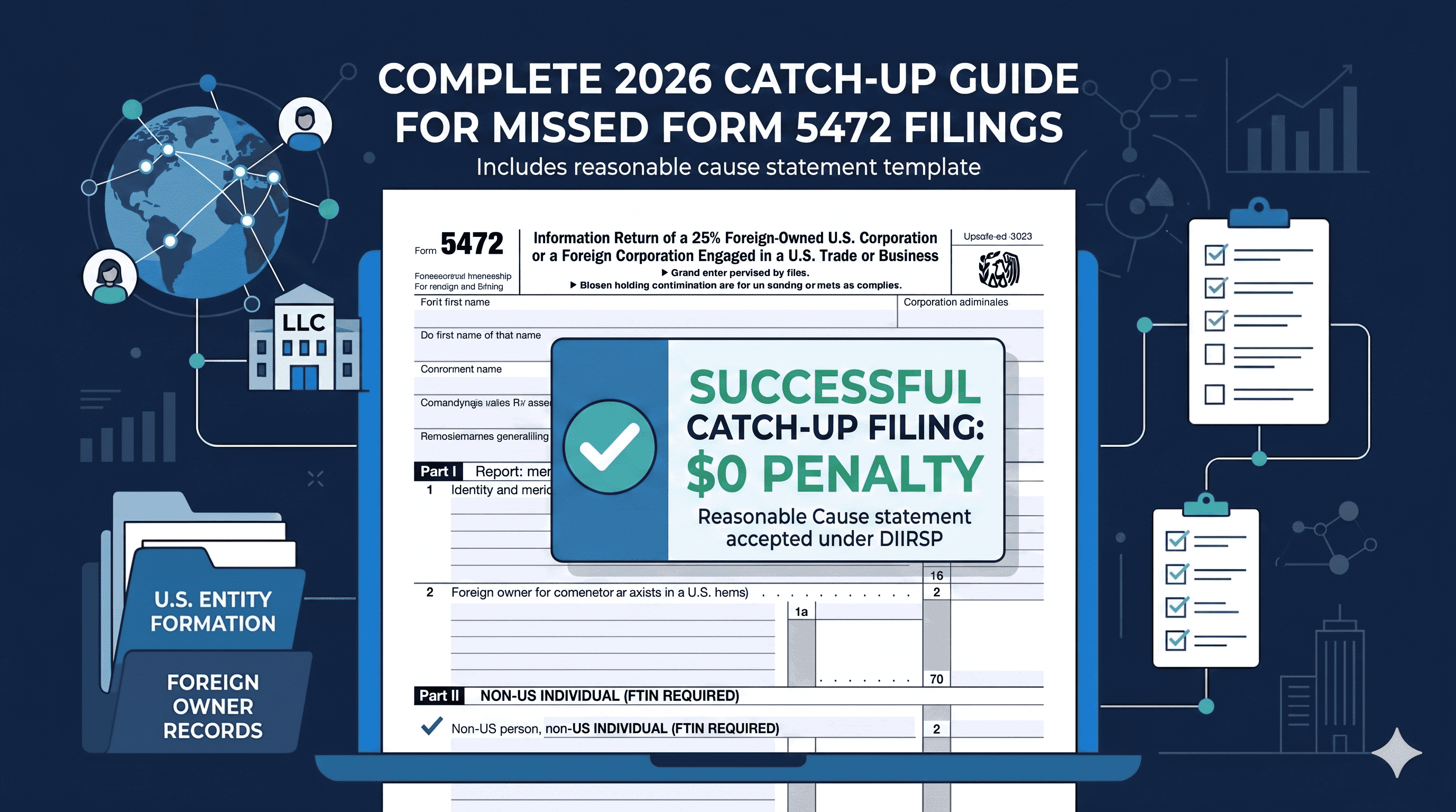

But here's the part nobody mentions: the IRS has a specific, well-documented process for foreign founders who failed to file because they didn't know the requirement existed. It's called the Delinquent International Information Return Submission Procedure (DIIRSP), and when used correctly, it results in zero penalties in many cases.

How the IRS handles late Form 5472 filings

The IRS has three primary tracks for late international information returns:

Track 1 — Pre-discovery filing with reasonable cause (DIIRSP). You file the missing forms voluntarily before the IRS contacts you, with a written reasonable cause statement. If accepted, no penalty is assessed.

Track 2 — Reasonable cause defense after IRS contact. You file the missing forms in response to an IRS notice, with a reasonable cause statement. The IRS may or may not accept; penalties may be partially or fully abated.

Track 3 — No reasonable cause / IRS enforcement. You file (or don't file) after IRS contact without adequate reasonable cause. Penalties are assessed: $25,000 per form, per year, plus continuation penalties of $25,000 every 30 days after the 90-day notice period.

Your goal is to stay on Track 1. The Delinquent International Information Return Submission Procedure exists specifically for foreign founders who didn't know they had a filing requirement.

What is the Delinquent International Information Return Submission Procedure?

The DIIRSP is an IRS procedure that allows taxpayers to file delinquent international information returns (including Form 5472, Form 5471, Form 8865, and others) without automatic penalty assessment if they:

- File the missing returns voluntarily, before any IRS contact

- Attach a written reasonable cause statement

- Demonstrate they exercised ordinary business care and prudence

The IRS specifically designed this procedure for taxpayers who:

- Were not aware of the filing requirement

- Relied on incorrect professional advice

- Had administrative or clerical failures

- Faced circumstances beyond their reasonable control

For foreign founders, "I didn't know foreign-owned LLCs had to file an IRS form even with zero income" is a recognized basis for reasonable cause — especially given that the requirement was only expanded to disregarded entities in 2017 and is poorly publicized.

What qualifies as "reasonable cause"?

The IRS uses a fact-and-circumstances test. Reasonable cause exists when you can show you exercised ordinary business care and prudence but were still unable to comply.

Generally accepted reasonable cause grounds for foreign founders

- Lack of awareness due to recent rule change. Form 5472 was expanded to foreign-owned disregarded entities only in 2017. Many founders formed LLCs based on advice or information that predated this change.

- Reliance on incorrect professional advice. If your registered agent, LLC formation service, or initial CPA told you no filing was required, this can establish reasonable cause.

- Foreign founder status with limited US tax knowledge. The IRS recognizes that non-US persons often don't have access to US tax guidance.

- No US tax liability and no notice of obligation. Many founders assume "no income = no filing" because that's how taxes work in most countries.

- Administrative errors or transitional events. Death of an advisor, business disruption, illness, or natural disasters can establish reasonable cause.

- First-time filer status. A newly-formed LLC's first year filing failure is sometimes treated more leniently than chronic non-filers.

What does NOT qualify as reasonable cause

- "I didn't have the money to hire a CPA" (not a reasonable cause)

- "I was too busy" (not a reasonable cause)

- "I forgot" (not a reasonable cause)

- "I knew about the requirement but didn't think the penalty would apply" (willful non-filing)

- Generic statements without specific facts

The key distinction: reasonable cause requires that you tried in good faith to comply or genuinely didn't know there was something to comply with. Knowing about the rule and choosing not to file is willful non-compliance, which receives no relief.

Step-by-step: how to file catch-up Form 5472

- Identify every missed year. Pull formation records and bank statements for every year your LLC existed. Each year is a separate filing.

- Gather supporting documents for each year. Bank statements, formation documents, EIN confirmation, owner identification, prior IRS correspondence (if any).

- Reconstruct reportable transactions for each year. Go through each year's transactions and identify all monetary movements between the LLC and the foreign owner.

- Generate Form 5472 + pro forma Form 1120 for each year. Each year needs its own complete filing package. Use the year-appropriate version of the form.

- Draft the reasonable cause statement. This is the single most important document in the catch-up filing. Template below.

- Compile the package. Form 5472, pro forma Form 1120, reasonable cause statement (signed), supporting evidence, cover sheet.

- Mail or fax to the correct IRS address. Mail: IRS, 1973 Rulon White Blvd, M/S 6112, Attn: PIN Unit, Ogden, UT 84201. Fax: 855-887-7737. Use certified mail with return receipt.

- Keep copies of everything. Scanned copies, certified mail receipt, fax confirmations, subsequent IRS correspondence. Retain for at least 7 years.

- Monitor for IRS response. Most catch-up filings result in no response (silent acceptance). If the IRS sends a notice, respond promptly with a tax professional.

Reasonable Cause Statement Template

Below is a template you can adapt for your situation. Modify it to reflect your actual facts — generic copy-paste statements are easier for the IRS to reject. The strongest reasonable cause statements are specific, factual, and document-supported.

REASONABLE CAUSE STATEMENT FOR LATE FILING OF FORM 5472

Tax Year: [Year]

LLC Name: [Your LLC Legal Name]

EIN: [Your EIN]

State of Formation: [State]

Foreign Owner Name: [Your Full Legal Name]

Foreign Owner Country of Residence: [Country]

Dear Internal Revenue Service:

I am submitting this delinquent Form 5472 and accompanying pro forma Form 1120 for tax year [YEAR] for [LLC NAME], EIN [EIN], pursuant to the Delinquent International Information Return Submission Procedure. I respectfully request that no penalty be assessed under IRC §6038A(d) based on the reasonable cause described below.

Background of the Entity

I am [YOUR FULL NAME], a citizen and resident of [COUNTRY]. I am the sole owner of [LLC NAME], a single-member limited liability company organized under the laws of the State of [STATE] on [DATE OF FORMATION]. The LLC is treated as a disregarded entity for US federal income tax purposes. I am not a US citizen, US resident, or US person under IRC §7701.

Reason for the Late Filing

[Choose and adapt one or more of the following based on your actual circumstances:]

Option A — Lack of awareness due to status as foreign founder:

At the time I formed this LLC, I was not aware that a foreign-owned single-member LLC treated as a disregarded entity for income tax purposes was nonetheless required to file Form 5472 with a pro forma Form 1120 each year, regardless of whether the LLC had income. My understanding, based on common information about disregarded entities in the foreign founder community and information available at the time of formation, was that no US tax filing would be required if the LLC had no US-source income or US-effective trade or business activity.

Option B — Reliance on incorrect advice:

At the time of formation, I relied on [SPECIFY: e.g., my LLC formation service / my registered agent / a CPA I consulted / online guidance], which did not inform me of the Form 5472 filing requirement for foreign-owned disregarded entities. I had no reason to doubt this advice at the time.

Option C — Recent expansion of the rule:

The Form 5472 filing requirement was expanded to foreign-owned domestic disregarded entities only by Treasury Regulations effective for tax years beginning on or after January 1, 2017. As a foreign individual with limited access to US tax compliance information, I was not aware of this rule change.

Actions Taken Upon Discovery

Upon learning of the Form 5472 requirement on [DATE OF DISCOVERY], I [DESCRIBE THE STEPS TAKEN]. I am submitting this filing voluntarily, before any contact from the Internal Revenue Service, in good faith and with the intent to fully comply with all applicable obligations going forward.

Ordinary Business Care and Prudence

I exercised ordinary business care and prudence by [DESCRIBE]. The failure to file Form 5472 was not willful and did not result from neglect, but rather from an absence of awareness that this specific filing requirement applied to my situation.

Going-Forward Compliance

I have implemented [DESCRIBE] to ensure timely filing of all required forms going forward. I am committed to full compliance with all Internal Revenue Service requirements applicable to my entity.

Request for Relief

Based on the foregoing facts and circumstances, I respectfully request that the Internal Revenue Service accept this delinquent Form 5472 under the Delinquent International Information Return Submission Procedure without assessment of penalty under IRC §6038A(d).

I declare under penalty of perjury that the foregoing is true and correct to the best of my knowledge and belief.

Signed: ______________________

Name: [YOUR FULL NAME]

Date: [DATE]

Capacity: Sole Member of [LLC NAME]

Critical drafting notes

- Be specific. Generic statements get rejected. Name the formation service, name the dates, name the documents you relied on.

- Attach supporting evidence where possible. If you relied on incorrect advice, attach the written advice or email.

- Don't admit willful conduct. Avoid language like "I knew but didn't think it mattered" or "I delayed filing because..."

- One statement per missed year. Each missed year is a separate filing with its own reasonable cause statement.

- Have a tax professional review if possible. A US-licensed CPA or tax attorney can spot weaknesses before the IRS does.

How long does the IRS take to respond?

There's no fixed timeline. Based on aggregated practitioner reports:

- No response within 90 days: Most common outcome. Silent acceptance.

- Response within 90-180 days: Sometimes a CP notice requesting clarification or rejecting the reasonable cause.

- Response within 6-18 months: Penalty notice (CP15 or CP215) if reasonable cause was insufficient or not provided.

- No response within 2 years: Effectively accepted; matter closed.

If you receive an IRS notice during this period, respond promptly with the help of a tax professional. Do not ignore IRS correspondence.

What if your reasonable cause is rejected?

If the IRS rejects your reasonable cause and assesses penalties, you have several options:

- Appeal the determination. You generally have 30 days from the notice date to file an appeal.

- Form 843 — Claim for Refund and Request for Abatement. File a separate request with additional facts and documentation.

- Tax Court petition. If administrative appeals fail, you may petition the US Tax Court within the statutory deadline.

- Collection Due Process hearing. If the IRS begins collection actions, request a CDP hearing.

- Offer in Compromise. If penalties are assessed and upheld but you cannot pay, an Offer in Compromise may settle the liability for less than the full amount.

All of these are best handled with a US-licensed tax professional, especially if penalties exceed $10,000.

The "stack and panic" mistake — don't do this

Some foreign founders, after discovering missed filings, file all missed years at once with a single combined reasonable cause statement, hoping the IRS treats them as one issue. This usually backfires.

Each missed year is a separate failure to file. Each requires its own complete filing package and its own reasonable cause statement. Trying to combine them:

- Confuses IRS processing centers

- Triggers automated penalty assessment systems that process per-year

- Can be interpreted as a single "course of conduct" failure (worse than separate year failures)

- Makes it harder to show specific facts justifying each year's failure

File them as separate packages. Mail them on the same day if you want, but treat each year as its own complete filing.

Common catch-up filing mistakes

- Filing for some missed years but not all. This signals to the IRS that you're aware of the obligation, which weakens reasonable cause for the years you didn't file.

- Filing the current year first, then prior years later. This timing pattern often triggers IRS scrutiny. File prior years first.

- Using the wrong year's version of Form 5472. Each tax year has its own form revision. Using the current form for an old year creates rejection risk.

- Forgetting the pro forma 1120. Form 5472 alone is treated as a failure to file.

- Mailing to the wrong IRS address. Use the Ogden, UT MS 6112 address specifically.

- Skipping the reasonable cause statement. Without it, you've simply filed a late return, and penalties auto-assess.

- Generic, template-copy reasonable cause statements. The IRS sees thousands of these. The strongest statements are specific, factual, and document-supported.

When should you hire a professional vs. DIY?

DIY is reasonable when

- You missed 1-2 years

- The LLC had simple finances (one bank account, basic transactions)

- You're comfortable assembling the filing package

- Total penalty exposure is under ~$30,000

- You're filing proactively (before IRS contact)

- You can craft a specific, factual reasonable cause statement

Get professional help when

- You missed 3+ years

- The LLC has complex transactions (multi-entity, treaty positions, transfer pricing)

- You've already received an IRS notice

- Total penalty exposure exceeds $50,000

- You face additional complications (FinCEN BOI, FBAR, state taxes)

- The reasonable cause case requires legal interpretation

- You're not confident in your record-keeping for prior years

A US-licensed CPA or tax attorney familiar with cross-border compliance typically charges $500-2,000 per year of catch-up filing.

Frequently Asked Questions

Will I definitely avoid penalties by filing late with reasonable cause?+

There is no guarantee. The IRS has discretion in accepting or rejecting reasonable cause. However, foreign founders who file proactively (before IRS contact) with specific, documented reasonable cause have historically obtained relief in the majority of cases.

How many years back do I need to file?+

File for every year the LLC existed and had reportable transactions, including years with only an initial capital contribution. The IRS does not have a statute of limitations on unfiled returns.

What if I can't reconstruct old bank statements?+

Most banks (Mercury, Stripe, Wise, Bank of America, Chase) can provide 5-7 years of historical statements on request. For older records, contact the bank directly.

What if my LLC has been dissolved?+

You still owe Form 5472 for each year the LLC existed. Dissolution does not extinguish prior-year filing obligations. The IRS treats these the same as active entity filings.

Do I need an ITIN to file catch-up Form 5472?+

The LLC files using its EIN, not the owner's identifying number. Since 2026 OBBBA changes, the foreign owner's FTIN (typically a home-country tax ID) is required on the form. An ITIN is not required.

Can I file catch-up returns electronically?+

No. Foreign-owned disregarded entities cannot e-file Form 5472. Each year's package must be mailed or faxed to the special IRS address.

What happens if I already received an IRS notice?+

Respond immediately, ideally with the help of a US-licensed tax professional. Your reasonable cause argument is harder once IRS contact has occurred, but not impossible. Do not ignore IRS correspondence — collection actions can escalate quickly.

Can the IRS criminally prosecute Form 5472 non-filing?+

In theory, yes — willful failure to file information returns can carry criminal penalties. In practice, criminal prosecution is extremely rare for Form 5472 non-filing absent additional indicators of fraud. The civil penalty ($25,000+) is the realistic exposure.

Should I file Form 5472 before or after the current year's filing?+

File prior-year catch-ups first, ideally a week or two before the current year. This sequence signals to the IRS that you've identified and corrected past failures before adding the current year.

Is the reasonable cause template guaranteed to work?+

No template can guarantee acceptance. The strongest reasonable cause statements are customized to specific facts and supported by documentation. Generic, unmodified template language is one of the most common reasons reasonable cause is rejected.