Form 5472 for Foreign-Owned LLCs: The Complete 2026 Guide

Complete 2026 guide to IRS Form 5472 for foreign-owned US LLCs, including filing rules, deadlines, penalties, pro forma Form 1120, and common mistakes.

Finvio Editorial Team

Foreign-Owned LLC Compliance Research

•11 min read •Reviewed by US-licensed CPA partner

Quick Answer

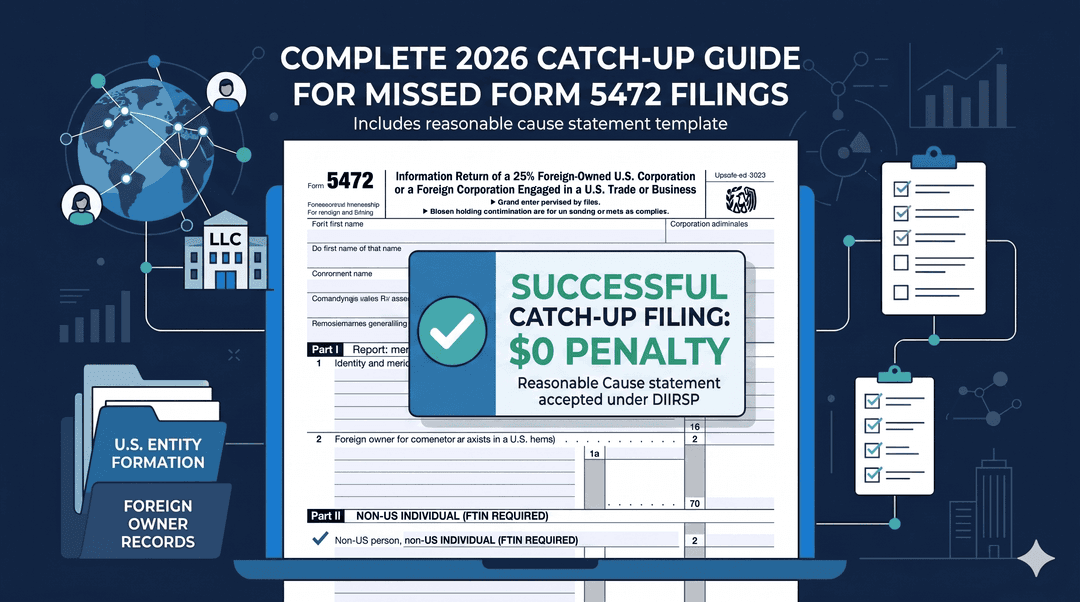

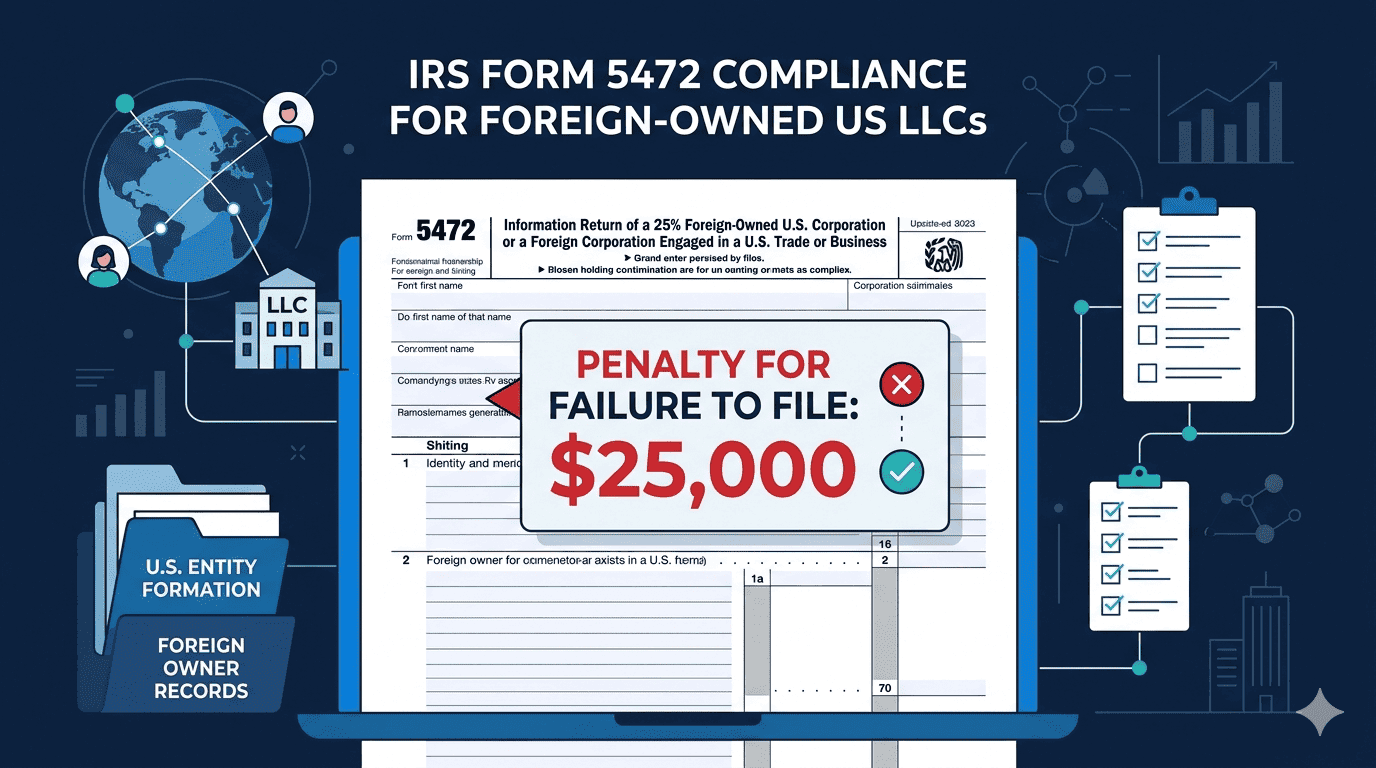

Foreign-owned single-member US LLCs must file Form 5472 with a pro forma Form 1120 every year, even when the LLC had zero income. The deadline for the 2025 tax year is April 15, 2026, extendable to October 15, 2026 by filing Form 7004. The penalty for missing or incomplete filing is $25,000 per form, per year, with no statutory cap under IRC §6038A(d)(1). After 90 days of IRS notice, an additional $25,000 stacks every 30 days. Electronic filing is not available — disregarded entities must mail or fax the package to the IRS Ogden, UT center. Capital contributions, owner withdrawals, and inter-company transfers are all reportable transactions.

⚠ The most expensive mistake: foreign founders assume "disregarded entity" means no IRS filing. The opposite is true. Since 2017, single-member LLCs owned by non-US persons must file Form 5472 regardless of revenue.

What Form 5472 actually is

Form 5472 is an information return required under IRC §6038A and §6038C. It is not a tax payment form. It exists so the IRS can monitor money flowing between US entities and their foreign owners or related parties.

The form requires disclosure of:

- The reporting corporation (your LLC)

- The foreign related party (you, as owner)

- All monetary transactions between them

- Capital contributions and distributions

- Loans, interest, and non-monetary transactions

Before 2017, only corporations filed Form 5472. That changed with the Tax Cuts and Jobs Act of 2017, which expanded the requirement to all foreign-owned disregarded entities including single-member LLCs.

Who must file Form 5472 in 2026

You must file Form 5472 if any of the following are true:

- You own a US single-member LLC that's 100% owned by a non-US person or non-US company

- Your US corporation has 25% or more foreign ownership (direct or indirect)

- You're a foreign corporation engaged in a US trade or business

- You're part of a multi-tier international structure with cross-border transactions

The most common case — and the one that traps the most founders — is the foreign-owned single-member LLC formed in Wyoming, Delaware, New Mexico, or Florida.

Examples of who must file

- An Indian founder owns 100% of a Wyoming LLC selling SaaS to US customers

- A Sri Lankan freelancer owns a Delaware LLC for invoicing US clients

- A Brazilian e-commerce seller owns a Florida LLC for Amazon US sales

- A Pakistani SaaS founder owns a Wyoming LLC with one US bank account and a Stripe connection

- A UAE-based investor owns 30% of a Delaware C-Corp with US operations

Who does not file Form 5472

- US citizens or US residents who own a US LLC (even if living abroad)

- US LLCs owned by other US persons

- LLCs taxed as partnerships (multi-member LLCs file Form 1065 instead)

- LLCs that elected S-Corp status

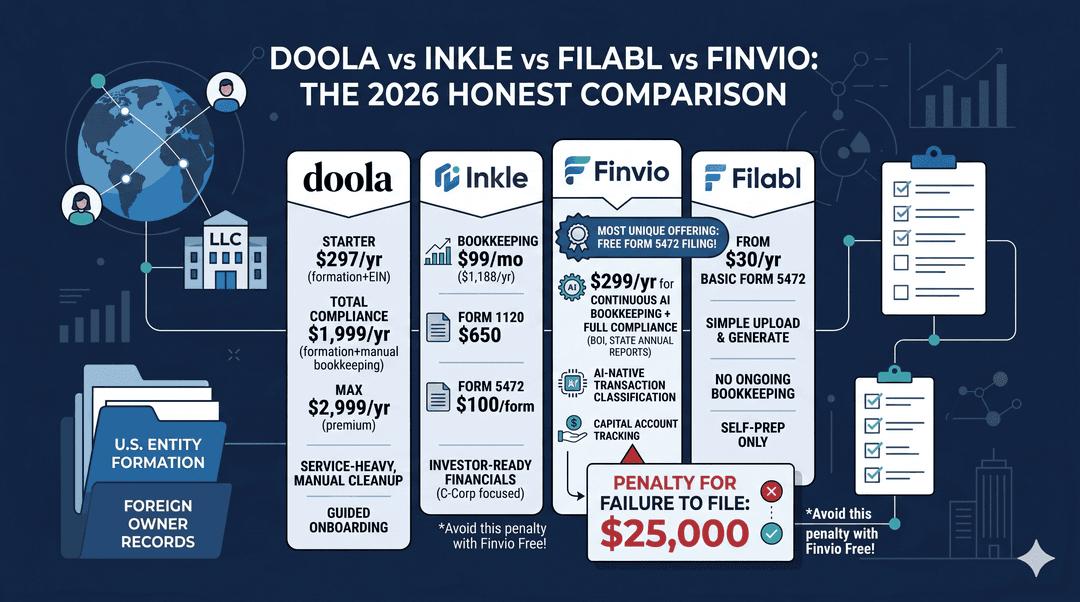

The $25,000 penalty — how it actually works

The base penalty for failing to file a complete and correct Form 5472 is $25,000 per form, per tax year, under IRC §6038A(d)(1). This penalty applies whether you filed nothing, filed incorrectly, or filed substantially incomplete information.

If the IRS sends a notice of non-compliance and you don't fix the failure within 90 days, an additional $25,000 stacks every 30 days thereafter — with no maximum cap under IRC §6038A(d)(2).

Real penalty math

Suppose a foreign founder missed filing Form 5472 in 2023. The IRS sends a notice on March 1, 2026. The founder doesn't respond. By September 1, 2026, the situation looks like:

- Base penalty: $25,000

- 90-day grace period ends June 1, 2026

- Three 30-day periods elapsed by September 1: 3 × $25,000 = $75,000

- Total: $100,000 for one missed filing

Multiple related parties multiply the penalty further. Multiple missed years compound. There is no statute of limitations.

When is the 2026 deadline?

For a calendar-year foreign-owned LLC reporting the 2025 tax year:

- Original deadline: April 15, 2026

- Extended deadline (with Form 7004): October 15, 2026

For Form 7004, enter the Form 1120 code in Part I, line 1, and write "Foreign-owned U.S. DE" across the top. Send to fax 855-887-7737 or mail to the Ogden, UT address.

The pro forma Form 1120 explained

A foreign-owned single-member LLC does not file a normal corporate income tax return. Instead, it files a "pro forma" Form 1120 — a stripped-down version that exists only as a wrapper for Form 5472.

The pro forma 1120 only requires basic entity information:

- Entity name and address

- EIN

- Date of formation

- "Foreign-owned U.S. Disregarded Entity" written across the top

- Form 5472 attached

You do not calculate taxable income on the pro forma 1120. You do not report revenue or expenses on Schedule C. The form exists solely so Form 5472 has something to attach to.

How to file Form 5472: step-by-step

- Confirm you need to file. Verify you're a foreign-owned disregarded entity. If you have any reportable transactions — including the initial capital contribution — you must file.

- Get your EIN. The LLC needs an EIN before filing. Foreign owners without an SSN or ITIN can obtain an EIN by filing Form SS-4 with the IRS by fax. Allow 4-8 weeks.

- Identify all reportable transactions. Capital contributions, distributions, loans, inter-company transfers. Even non-monetary transactions count.

- Complete Form 5472. Fill in Part I (reporting corporation), Part II (25% foreign shareholder), Part III (related party), Part IV (monetary transactions), Part V (transactions for foreign-owned disregarded entities), and Part VI (non-monetary).

- Prepare the pro forma Form 1120. Fill in only entity-level information. Leave Schedule C and income calculations blank. Write "Foreign-owned U.S. DE" across the top.

- Assemble the package. Form 5472 must be attached to the pro forma Form 1120. Submitting them separately is treated as a failure to file.

- Mail or fax to the IRS. Mail: Internal Revenue Service, 1973 Rulon White Blvd, M/S 6112, Attn: PIN Unit, Ogden, UT 84201. Fax: 855-887-7737.

- Keep records. Retain documentation and proof of mailing/fax for at least three years.

Electronic filing is not available

This is the single most-misunderstood rule. Foreign-owned disregarded entities cannot e-file Form 5472. The only acceptable methods are paper mail (USPS certified mail is recommended) or fax to the IRS Ogden processing center.

If your tax software offers to e-file Form 5472 for your LLC, it's either filing incorrectly or you're not actually a disregarded entity.

What counts as a reportable transaction?

A reportable transaction is any monetary or non-monetary transaction between the LLC and a foreign related party.

Money flowing into the LLC (Part V — Owner Contributions)

- Initial capital deposit when the LLC was funded

- Subsequent owner contributions to fund operations

- Loans from the foreign owner to the LLC

- Personal expenses paid by the owner on behalf of the LLC

Money flowing out of the LLC (Part V — Distributions)

- Owner withdrawals or "draws" to the foreign owner's personal account

- Loan repayments to the foreign owner

- Profit distributions wired to a foreign account

- Payments to a foreign-owned related entity

Non-monetary transactions (Part VI)

- Services provided by the owner to the LLC without billing

- Use of the owner's IP, software, or assets by the LLC

- Assets transferred between the LLC and owner

A zero-revenue LLC that received only an initial capital contribution still has a reportable transaction (the contribution itself) and must file Form 5472.

The 2026 OBBBA changes affecting foreign-owned LLCs

The One Big Beautiful Bill Act (OBBBA), signed July 2025, introduced several provisions starting in 2026:

- New 1% remittance excise tax on certain cross-border money transfers from US accounts to foreign accounts

- FTIN requirements — Foreign Taxpayer Identification Numbers now requested for all foreign owners of US disregarded entities

- FDDEI transfer pricing changes that may affect inter-company pricing structures

- Updated FinCEN beneficial ownership reporting layered on top of existing Form 5472 obligations

The 7 most expensive Form 5472 mistakes

- Not knowing the form exists. Foreign founders form a Wyoming LLC, run revenue through Stripe and Mercury, and never realize they have a filing obligation.

- Filing Form 5472 without the pro forma Form 1120. Submitting Form 5472 alone is treated as a failure to file and triggers the full $25,000 penalty.

- Sending the filing to the wrong address. The standard Form 1120 filing address is not where foreign-owned DEs send their packages.

- Filing electronically when you can't. Disregarded entities cannot e-file. Some tax software offers this option in error.

- Skipping the filing because the LLC had no revenue. A zero-revenue LLC with an initial capital contribution still has a reportable transaction.

- Combining multiple related parties on one form. If you have three foreign related parties, you file three separate Forms 5472.

- Missing the deadline and assuming "I'll file next year." Each year of non-filing is a separate $25,000 penalty.

Form 5472 vs Form 5471 — which do you file?

These are two different forms with opposite triggers:

| Who files | US entity with 25%+ foreign ownership; foreign-owned single-member LLC | US person who owns interest in a foreign corporation |

| Direction | US entity reports about foreign related parties | US owner reports about foreign company |

| Common scenario | Pakistani founder owns Wyoming LLC | US citizen owns 25% of a UK company |

| Penalty | $25,000 per form per year | $10,000 per form, escalating to $50,000 |

Frequently Asked Questions

Does a foreign-owned LLC with zero income need to file Form 5472?+

Yes. A foreign-owned single-member LLC must file Form 5472 if it had any reportable transaction during the year, including an initial capital contribution, even if the LLC generated zero income.

Can Form 5472 be filed electronically?+

No. Foreign-owned disregarded entities cannot e-file Form 5472. The form must be mailed or faxed to the IRS Ogden, Utah processing center together with a pro forma Form 1120.

What is the penalty for missing Form 5472?+

The penalty for failing to file a complete and correct Form 5472 is $25,000 per form, per year. Additional penalties may apply every 30 days after an IRS notice if the failure is not corrected.

Does a foreign owner need an ITIN to file Form 5472?+

No. Form 5472 is filed using the LLC’s EIN. A foreign owner generally does not need an ITIN solely for Form 5472 filing purposes.